The Commercial Real Estate Crisis is not just a looming threat; it is becoming a reality for many investors and banks as high office vacancy rates negatively impact the economy. The surge in vacant office spaces, a consequence of changing work dynamics post-pandemic, has left significant repercussions for property values and the financial sector. Analysts, like Kenneth Rogoff, emphasize that the high volume of real estate loans maturing by 2025 could spell trouble for banks, potentially leading to bank failures if delinquencies rise. With the economic downturn forcing many firms to reevaluate their portfolios, the commercial real estate sector finds itself in a precarious position that could have a domino effect on the broader economy. Navigating this crisis will require astute awareness of market conditions and regulatory responses to safeguard against a deeper financial fallout.

In recent times, the commercial property market has faced considerable challenges, often referred to as a real estate downturn. This sector’s struggles stem from factors such as rising office vacancies and increased pressure on financial institutions due to outstanding real estate loans. The interconnectedness of commercial property and banking has raised concerns about the potential repercussions of bank failures amid this adverse environment. As economic uncertainties grow, the effects on lenders and the overall financial landscape become increasingly pronounced, warranting a closer examination of the implications for the economy at large.

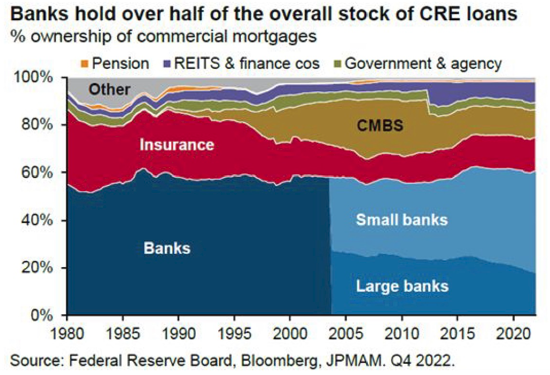

The Current State of Commercial Real Estate

As businesses navigate post-pandemic recovery, high office vacancy rates have emerged as a significant barrier to the commercial real estate market’s resurgence. In major U.S. cities, vacancy rates soar between 12% and 23%, resulting in substantial depreciation of property values. This downturn has not only shaken investor confidence but has caused alarm among banks holding a large portfolio of real estate loans. The impact on financial institutions is particularly concerning as a substantial portion of commercial mortgage debt is set to mature by 2025, which could exacerbate the financial strain on banks if widespread defaults occur.

The commercial real estate sector, once touted as a robust investment opportunity, is now teetering on the brink of crisis. With high office vacancy rates continuing to cast a shadow over property values and economic growth, the repercussions could ripple through the banking system. Kenneth Rogoff’s insights underscore the urgency of addressing these challenges, as the health of the commercial real estate market plays a pivotal role in broader economic stability.

Frequently Asked Questions

How might high office vacancy rates affect the commercial real estate crisis?

High office vacancy rates are a major contributing factor to the ongoing commercial real estate crisis. They depress property values and lead to financial strain on investors and owners, which can result in increased defaults on commercial real estate loans. As more offices remain vacant, the negative impact on the economy could escalate, driving banks to tighten lending practices and potentially triggering wider financial instability.

What is the expected impact of delinquent commercial real estate loans on banks during the ongoing crisis?

The current commercial real estate crisis, exacerbated by high vacancy rates and economic downturn, poses significant risks to banks holding commercial real estate loans. Delinquent loans could lead to substantial financial losses for smaller and regional banks, which may not withstand the pressure without appropriate capital buffers. This scenario could inflict wider damage on the banking sector, contributing to potential bank failures.

Will the commercial real estate crisis lead to a repeat of the 2008 financial meltdown?

While the commercial real estate crisis shares similarities with prior financial downturns, experts like Kenneth Rogoff suggest it won’t necessarily lead to a repeat of the 2008 meltdown. The current situation, characterized by high office vacancy rates and looming loan maturities, could lead to some losses in the banking sector; however, the overall economic outlook remains relatively stable. Major banks are better regulated post-2008, which may mitigate the risk of a total systemic failure.

How does the economic downturn influence the commercial real estate crisis?

The economic downturn directly contributes to the commercial real estate crisis by reducing demand for office spaces, resulting in higher vacancy rates. As businesses adopt more remote work, the need for physical offices diminishes, driving property values down and straining real estate loans. This cycle can lead to increased defaults, impacting banks’ solvency and potentially creating a ripple effect throughout the economy.

What role do banks play in the commercial real estate crisis?

Banks play a crucial role in the commercial real estate crisis by providing loans to investors and businesses in this sector. With high office vacancy rates continuing to strain property values, banks face greater risks from potential defaults on these real estate loans. Consequently, the financial health of banks will significantly influence the wider economy as regional banks, heavily invested in commercial real estate, may struggle to recover from losses, impacting their lending capacity.

What should investors know about the commercial real estate crisis and its implications?

Investors should be aware that the commercial real estate crisis is currently characterized by high vacancy rates and increasing pressure on real estate loans. As the economy faces potential downturns, the viability of commercial properties may be compromised, leading to financial losses. It’s essential for investors to assess the risks involved and consider diversifying their portfolios to mitigate impacts associated with potential bank failures linked to the crisis.

How could commercial real estate loan defaults affect consumers?

Defaults on commercial real estate loans can have a trickle-down effect on consumers. As regional banks face financial distress due to high vacancy rates and bad debts, they may tighten lending standards or reduce credit availability. This could lead to higher borrowing costs for consumers, reduced spending power, and a slowdown in economic activity, ultimately impacting job markets and consumer confidence.

| Key Point | Details | |

|---|---|---|

| High Office-Vacancy Rates | Vacancy rates range from 12% to 23% in major cities, affecting property values. | |

| Commercial Real Estate Debt | 20% of $4.7 trillion in mortgage debt is due this year, raising risks for banks. | |

| Potential for Bank Losses | Experts believe losses won’t lead to a full-blown financial crisis but may impact smaller banks. | |

| Economic Outlook | Despite challenges, the overall economy remains relatively strong with a healthy job market and stock market. | |

| Primary Causes of Crisis | High leveraging of real estate investments and pandemic-induced demand drop for office space. | |

| Impact on Consumers | Potential hardships for regional banks could affect consumers through tighter lending and reduced consumption. | |

| Preparedness of Major Banks | Large banks remain insulated due to diversification and high interest income, unlike smaller banks. | |

| Outlook for the Future | A major recession would exacerbate the crisis, but currently, the risks are manageable within larger banks. | |

Summary

The Commercial Real Estate Crisis is a significant concern as high vacancy rates threaten to destabilize the economy. Despite fears of widespread bank failures, experts suggest that while many companies may incur substantial losses, a systemic crisis is unlikely. The primary factors contributing to this dilemma include excessive leverage in real estate, compounded by reduced demand for office spaces since the pandemic. Furthermore, regional banks face potential vulnerabilities, but larger banks, benefiting from diversification and strong financial regulations, are better positioned to withstand these pressures. To navigate this crisis effectively, a proactive approach in addressing the rising interest rates and supporting stressed assets will be crucial.