As we approach the contentious landscape of corporate tax rates in 2025, the debate surrounding their potential increases or further cuts is intensifying. The expiration of key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) will undoubtedly set the stage for a fierce political battle. With the Child Tax Credit also on the line, voters are paying close attention to how these changes could affect their personal finances. Harvard economist Gabriel Chodorow-Reich’s analysis sheds light on the implications of corporate tax cuts, revealing that while some benefits were seen, they were not substantial enough to offset the drastic drop in tax revenues. As legislators grapple with these complex issues, it’s clear that the 2025 tax battle will be a defining moment for U.S. fiscal policy.

In 2025, the focus on corporate income taxation will be more pressing than ever as key provisions from the significant 2017 tax reforms near their expiration dates. This pivotal period raises critical questions about the future of corporate levies amidst promising discussions likely to shape fiscal policy for years to come. Experts like Gabriel Chodorow-Reich are examining the impact of previous tax cuts and offering insight into how such reforms influenced investment and wage dynamics. The political arena is rife with contrasting perspectives, particularly when discussing the implications of the expiring Child Tax Credit alongside corporate taxation strategies. As stakeholders prepare for this upcoming economic recalibration, understanding the repercussions of corporate tax structures will be essential.

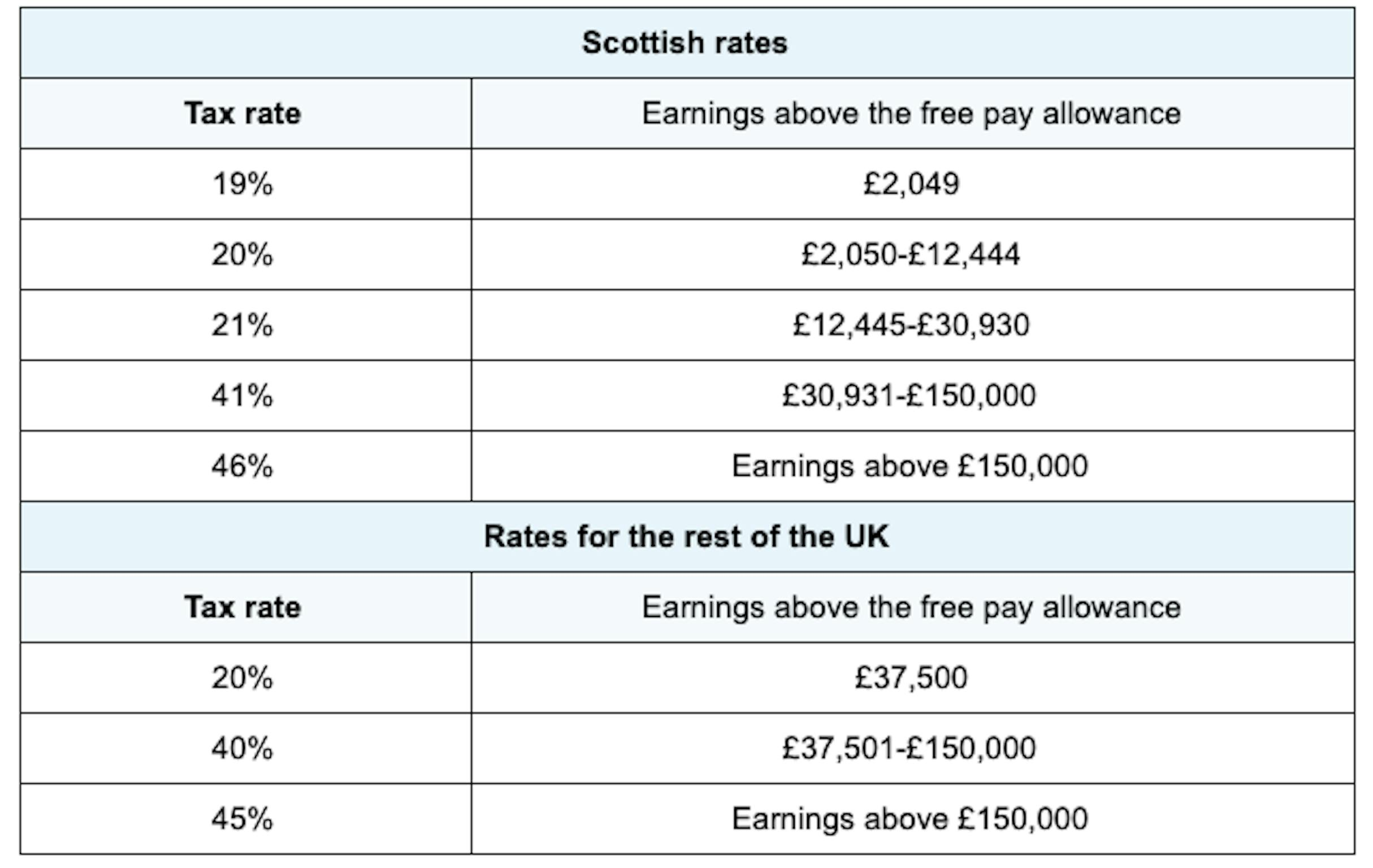

Understanding the Corporate Tax Rates 2025

As Congress prepares for a crucial tax battle in 2025, the topic of corporate tax rates has resurfaced at the forefront of economic discussions. The impending expiration of several key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) has ignited debates among lawmakers and economists alike. With proposals for increased corporate tax rates from Democrats, juxtaposed against Republican calls for further reductions, the discourse centers on how these changes could impact the overall economy. In 2025, the landscape of corporate taxation will play a pivotal role in shaping fiscal policy and its ripple effects on businesses and households across the nation.

The potential changes in corporate tax rates hinge on the findings from analyses conducted by economists like Gabriel Chodorow-Reich. His studies delve into the real-world implications of the TCJA, revealing that while corporate tax cuts were intended to stimulate economic growth, the actual financial outcomes showed limited effectiveness in enhancing wages and business investments. As expiration dates loom for crucial tax provisions, the conversation will likely shift towards weighing the benefits of maintaining lower rates against the necessity of restoring revenue channels that support public welfare, such as the Child Tax Credit.

Impact of TCJA: Gains and Losses

The Tax Cuts and Jobs Act significantly altered the corporate tax landscape by reducing the corporate tax rate from 35% to 21%. Advocates argued that these cuts were a necessary response to the U.S. becoming less competitive globally, as highlighted by Gabriel Chodorow-Reich in his analyses. While the TCJA was expected to boost wages and spur investment, the reality painted a more complex picture. Although there was a reported increase in investments, particularly in capital expenditures, the overall increase was modest when juxtaposed with the $100 billion annual revenue drop anticipated due to these cuts. As key provisions begin to sunset, the need for a nuanced understanding of what the TCJA achieved versus its failures takes center stage.

Political perspectives on TCJA continue to evolve, especially as more Americans weigh in on issues like the Child Tax Credit expansion, which may be jeopardized by looming votes. The societal push for equitable economic growth versus corporate profitability troubles ongoing debates. Economists have expressed mixed feelings on whether tax cuts fundamentally lead to greater levels of business investment or wage increases. With a clear divergence in opinions, the 2025 elections will serve as a referendum on the efficacy of the TCJA and the direction that corporate tax policy should take moving forward.

Corporate Tax Cuts and Their Socioeconomic Implications

Corporate tax cuts have been a contentious point in U.S. economic policy, with proponents arguing that lower rates lead to increased corporate investment and job creation. However, Gabriel Chodorow-Reich’s research challenges this notion, arguing that while the TCJA initially spurred a slight uptick in investments, the benefits did not equate to the loss of tax revenue. Additionally, the impact of these cuts on labor wages has been shown to be less substantial than promised. These findings suggest that the 2017 tax reforms might not suffice to drive sustainable economic growth without concurrent revenue-generating measures.

The long-term socioeconomic implications of corporate tax cuts touch directly on income inequality and public service funding. As corporate tax revenue declines, critical investments in education, healthcare, and infrastructure could suffer, ultimately impacting the middle and lower-income demographics harder. Adjustments to the corporate tax rates in 2025 will reflect not only economic growth strategies but also a more significant reckoning on how best to balance corporate interests with the public good—highlighting the importance of informed legislative action in the impending tax battle.

The 2025 Tax Battle: A Crossroads for Economic Reform

The lead-in to the 2025 tax battle signifies a pivotal moment for both economic policy and political theater. As major provisions of the TCJA approach expiration, lawmakers face competing interests: maintaining lowered corporate tax rates versus restoring needed revenues to support public programs like the Child Tax Credit. This battle encapsulates broader discussions on fiscal responsibility and economic equity. Economists and policymakers must navigate a myriad of perspectives, with many citing the urgency of reforming corporate tax policies in light of the research conducted by Gabriel Chodorow-Reich.

As the political landscape heats up for the 2025 elections, the discussions surrounding corporate tax rates will undoubtedly influence voter sentiment. Candidates will need to articulate clear strategies that balance business growth with societal needs, balancing the economic aspirations of corporations against the fiscal necessities of government programs. Irrespective of the outcomes, the 2025 tax battle will serve as a crucial test of legislative priorities and a reflection of the evolving values towards taxation in America—a moment where fundamental shifts could redefine the future of U.S. economic policy.

Child Tax Credit: Significance in the 2025 Tax Debate

The Child Tax Credit stands at a critical juncture as Congress approaches the 2025 tax debate, with its expanded provisions potentially expiring amidst the broader discussions stemming from the TCJA. Many families across the nation have benefited from the increased credit, which was designed to alleviate financial pressures for lower and middle-income households. As legislators grapple with corporate tax rates, the fate of the Child Tax Credit serves as a vivid reminder of the human impact of tax policy. Failure to extend this benefit could exacerbate the struggles of families already facing economic uncertainties.

Gabriel Chodorow-Reich’s research highlights the need for comprehensive tax reform—one that does not solely focus on corporate interests, but also emphasizes the well-being of all Americans. Political factions could see the impending negotiations surrounding the Child Tax Credit as an opportunity to reevaluate not only how tax revenues are generated but also how they are distributed. The 2025 tax battle, therefore, will not only test the durability of the TCJA’s provisions but also reflect fundamental beliefs about social responsibility in fiscal policy and the need to foster an equitable economic structure.

Evaluating Corporate Tax Policy: Lessons from the TCJA

In reviewing the implications of the TCJA, it becomes evident that corporate tax policy requires a dual approach—balancing incentives for businesses with the fiscal needs of the country. Economic evaluations, including those from Gabriel Chodorow-Reich’s team, indicate that while tax reductions can incentivize certain growth metrics, they often fail to deliver on broader expectations for wage growth and significant revenue generation. The upcoming 2025 deliberations signal a crucial opportunity for lawmakers to reconsider the structure of tax provisions in alignment with empirical evidence rather than ideological beliefs.

With significant budget deficits anticipated due to the corporate tax cuts instituted under the TCJA, the need for a more sustainable tax environment has emerged. Rogers must weigh the efficacy of maintaining lower tax rates against reintroducing expiring provisions that can spur genuine growth. Such discussions will require a keen understanding of past failures and successes, ensuring that lessons learned from the TCJA inform future tax政策 decisions—directing towards a balanced approach that addresses business requirements without sidelining the economic needs of average Americans.

Corporate Investment: Analyzing the Returns

Investments in corporate capital were a focal point of the TCJA, which aimed to boost economic growth by allowing companies to write off their investments immediately. Gabriel Chodorow-Reich’s analysis shows that while there was an uptick in capital investment of around 11%, these results must be viewed through the lens of overall economic performance and return on investment. Critics of the TCJA argue that without the restoration of expensing provisions and a strategic reevaluation of corporate tax rates, any gains made in investments could be negligible in terms of broad economic benefits.

As discussions heat up for 2025, understanding the dynamics of corporate investment becomes essential for lawmakers seeking to influence fiscal policy. Balancing corporate benefits with public needs challenges the notion that tax cuts alone drive business growth. If the focus shifts towards targeted investments informed by robust data and economic realities, there may be opportunities for legislation that catalyzes meaningful growth that can benefit both businesses and the society at large—aligning interests that have often been seen as opposed.

The Political Ramifications of Corporate Tax Decisions

Political implications of the corporate tax rates are becoming increasingly significant as 2025 approaches. With both major political parties staking their claims, the decisions made concerning corporate taxes will have direct consequences not just on fiscal revenue but also on the public perceptions of social equity. The heightened focus on tax restructuring could become a pivotal part of campaign agendas, with politicians using the narrative around corporate tax rates and the Child Tax Credit as powerful tools in garnering voter support.

The need to strike a balance between attracting businesses and ensuring adequate funding for public programs remains a key concern. The upcoming discussions will push candidates to articulate comprehensive strategies that address the multifaceted impact of tax policy. This dialogue represents not just the mechanics of tax rates but a broader ideological competition over what role government should play in the economy—a narrative that will resonate deeply with voters anticipating the 2025 elections.

Frequently Asked Questions

What are the projected impacts of Corporate Tax Rates in 2025 following the expiration of key TCJA provisions?

The impacts of Corporate Tax Rates in 2025 will largely depend on the reauthorization of provisions from the 2017 Tax Cuts and Jobs Act (TCJA) that are set to expire. Experts, including Gabriel Chodorow-Reich, suggest that the expiration could result in significant changes to corporate tax revenue and business investment, emphasizing that corporations responded to previous tax cuts with modest increases in investment. Hence, the 2025 tax battle will likely focus not just on tax rates but also on investment incentives.

How might the 2025 tax battle influence Corporate Tax Rates and the Child Tax Credit?

The 2025 tax battle is crucial as it centers on renewing or adjusting tax provisions established by the TCJA, which includes both Corporate Tax Rates and the Child Tax Credit. With many provisions set to expire, political debates are heating up. Advocates for retaining the Child Tax Credit argue for its renewal, while some policymakers propose raising corporate tax rates to fund other initiatives. Therefore, the 2025 tax discussion will significantly determine future economic strategies.

What are the implications of Corporate Tax Cuts from the TCJA as we approach 2025?

As we approach 2025, the implications of Corporate Tax Cuts from the TCJA are becoming clearer. While these cuts initially spurred temporary growth in business investments, Gabriel Chodorow-Reich’s research indicates that the benefits were modest compared to the substantial decline in tax revenues. This suggests that future considerations for Corporate Tax Rates will need to focus on the balance between stimulating investment and ensuring adequate government revenue.

Who is Gabriel Chodorow-Reich and why is his analysis important for understanding Corporate Tax Rates in 2025?

Gabriel Chodorow-Reich is a notable Harvard economist whose analysis of the TCJA provides critical insights into the effectiveness of Corporate Tax Rates and their relation to economic growth. His work challenges previous assumptions about the benefits of tax cuts and highlights the necessity of creating policies that not only incentivize investments but also address the revenue needs of the government as we head towards 2025.

What findings did Gabriel Chodorow-Reich present regarding the effects of corporate tax cuts before the 2025 tax reforms?

Gabriel Chodorow-Reich’s findings indicate that while corporate tax cuts from the TCJA did lead to some increase in business investments, the overall economic benefits were less than anticipated. His analysis shows that statutory rate reductions may not have significantly increased wage levels or corporate behavior, suggesting that lawmakers need to consider more comprehensive tax reforms as they prepare for 2025.

What does the term ‘2025 tax battle’ mean in the context of Corporate Tax Rates and fiscal policy?

The ‘2025 tax battle’ refers to the anticipated political and legislative discussions surrounding the renewal or adjustment of tax provisions established under the TCJA as they approach their expiration. This includes deliberations on Corporate Tax Rates and the Child Tax Credit, as policymakers from both parties negotiate potential reforms aimed at economic recovery and revenue generation.

| Key Points | Details |

|---|---|

| Corporate Tax Battle in 2025 | Congress is preparing for a debate over tax rates as parts of the 2017 Tax Cuts and Jobs Act expire. |

| Partisan Perspectives | Kamala Harris supports raising corporate rates for funding, while Donald Trump advocates for further cuts to stimulate growth. |

| Impact of TCJA Analysis | Gabriel Chodorow-Reich’s study highlights modest wage increases and investments but also significant revenue loss due to corporate tax rate cuts. |

| Corporate Tax Rate Changes | The TCJA lowered corporate tax rates from 35% to 21%, drastically decreasing federal tax revenue, projected at $100-150 billion loss annually. |

| Investment Impacts | Capital investments rose by 11% due to TCJA provisions allowing immediate expensing of investments, more effective than rate cuts alone. |

| Wage Increase Projections | Initial projections suggested wage growth up to $9,000 per employee, but actual increases were about $750 annually. |

| Future Corporate Tax Proposals | Chodorow-Reich suggests raising tax rates while restoring beneficial expensing provisions to increase investment and revenue. |

Summary

As we approach the discussions around Corporate Tax Rates 2025, it is essential to closely evaluate past tax legislation impacts. The upcoming tax battle will pivot on balancing the need for increased corporate tax revenues while ensuring that growth and investment are not stifled. With a notable decline in tax revenue observed from the TCJA and calls from various political factions for different approaches, the outcome of these debates will significantly shape economic policy and taxation strategies in the years to come.